Central Banking Today: I

The Fed

This article examines the evolution of the Federal Reserve from its founding as a lender-of-last-resort in 1913 to its current role as the central institution steering the global dollar system. We will look at how the Fed’s mandate, policy framework, and monetary tools have changed across different economic regimes — from the scarce reserves corridor system of the 20th century to today’s ample reserves framework shaped by quantitative easing and administered rates. The article further explores how these tools transmit through the financial system and why the structure of the Fed’s balance sheet has become central to modern monetary policy.

This is the first article in a broader series on contemporary central banking. The following pieces will examine how foreign central banks differ in their institutional design and policy implementation, before turning to several major debates in modern monetary theory — from the effectiveness of policy at the effective lower bound to questions surrounding alternative monetary regimes and structural problems in the U.S. Treasury market.

Institutional Background

The history of the central bank in the United States begins with the Federal Reserve Act of 1913. A series of banking panics preceding the act, most notably the Panic of 1907, exposed the inability of the financial system to deal with short bursts of liquidity stress on its own. Congress was therefore urged to find a systematic solution to this problem, and the Federal Reserve Act of 1913 became the answer. In its founding charter, the Fed was primarily envisioned as a lender-of-last-resort with broad powers to inject liquidity into the financial system in times of need. Organisationally, it was designed as a system of 12 regional banks representing the interests of the financial communities in different parts of the country. At the center of the system was (and still is) the Board of Governors, a federal agency based in Washington, D.C., which was expected to collate input on monetary issues from the regional branches and decide on the appropriate response.

The institutional design of the Fed became more clearly tied to monetary policymaking in the 1930s. In the context of the Great Depression, a more centralized decision-making body was needed so that open market operations would not be carried out in a fragmented and inconsistent manner across the regional banks. A major reform in 1935 established the Federal Open Market Committee, or FOMC, as the key body responsible for setting federal monetary policy. Its 12 voting members consist, to this day, of the 7 members of the Board of Governors, the president of the Fed’s New York branch, and 4 of the remaining 11 regional bank presidents, who vote on a rotating basis. This makes the FOMC the core committee through which monetary policy decisions are debated and implemented.

The implementation of monetary policy is driven through the Fed’s New York branch and specifically its Open Market Trading Desk division. Since its establishment in 1935, the desk has conducted open market operations on behalf of the Fed. The securities purchased through these operations are held in a portfolio called the System Open Market Account.

The Fed’s original financial stability mandate was expanded against the backdrop of persistent inflationary pressure of the 1970s. In 1977, Congress effectively codified the dual mandate, requiring the Fed to pursue both price stability and maximum employment as its targets. The following year, the Humphrey-Hawkins Act of 1978 added stronger reporting requirements, including regular reports to Congress and testimony by the Fed Chair on monetary policy objectives and economic conditions, helping to define the modern relationship between the Fed and the legislative body of the state.

Even though the law codified the dual mandate, it is up to the Fed to create guidelines around its objectives given different market circumstances and the implementation steps that can be used to achieve those objectives. The guidelines are officially called the Fed’s framework, while the implementation steps are more commonly known as the Fed’s policy tools.

The Fed’s Framework

The Fed’s framework has become an official part of the Fed’s institutional arrangement only in 2012. Before then, how the Fed reacted to different market conditions was uncodified and depended solely on the discretion of central bankers. Under Ben Bernanke’s leadership, the Fed committed to explicitly spelling out its operational framework and additionally decided to keep reviewing it regularly (every 5 years now) to ensure it sufficiently reflects any new structural changes in the economy.

The reason for the existence of the framework (whether a written one or an implicit one) itself is the need to clarify what levels the central bank should target with respect to inflation and employment, and how to act if those two objectives are in conflict.

The first framework review of 2012 codified the existing rules and named it flexible inflation targeting (FIT). Under FIT, the Fed has a 2% longer-run inflation goal, and relatively free hands in balancing inflation and employment when those two objectives conflict. It’s a framework that essentially codified the more discretionary approach used by central bankers since the 1980s.

The framework review that took place in 2020 was reacting to a very unique set of economic experiences that occurred in the previous decade. The 2010s saw an entrenched demand-side slump that persisted even as interest rates approached a practical floor, the so-called effective lower bound. The symptom of this was persistent sub-target inflation. Central banks went to great lengths to combat this and bring inflation back to its target, including major balance sheet operations intended to stimulate more investment in the economy.

Thus, the 2020 framework review aimed at specifically addressing the policy shortcomings of the previous framework. Officials at the Fed saw that the effect of persistently low inflation was that citizens’ inflation expectations became anchored at a much lower level than 2%. And just trying to hit the target again was not sufficient to offset that fait-accompli drop. Therefore, they proposed a so-called flexible average inflation targeting (FAIT), a new framework upgrading the previous one by taking into account the repercussions of extended low-inflation environments.

In the FAIT system, the central bank is supposed to tackle previous sub-target inflation by aiming to overshoot it in the future. Thus, on average over a longer horizon, inflation will be at 2%, while a short-term (quarterly) target might be much higher. Additionally, the framework allowed for higher employment levels (above the so-called estimated maximum employment in the economy) as long as inflation stayed stable. The central bank was only expected to intervene in case of employment shortfalls.

As a blow to the policymakers’ pursuits, the years following 2020 encumbered our economies with problems radically different from the previous decade. If the 2010s were dominated by a demand-driven slump, the 2020s seem to be dominated by supply-driven shocks. The pandemic shock, the Russian-Ukrainian crisis, and the current war in Iran are all forces pushing inflation up, which pressures central banks to raise interest rates to avoid inflation spiralling out of control. Thus, none of the advantages of FAIT seem to be actually useful in this new economic environment.

The Fed acknowledged this in its 2025 review and basically ditched inflation overshooting as its policy goal. It essentially returned to the pre-2020 FIT principles, stressing a more balanced, discretionary approach to resolving divergences between the labour market and price level that seem to have become a regular presence in this decade.

In addition to a more general framework that informs a qualitative direction of the Fed’s actions, monetary economists sometimes suggest incorporating more concrete formulas for informing the target interest rates of central banks. These are called policy rules and are mathematical formulations that derive optimal interest rate targets based on specific macroeconomic variables. The most famous of these is the so-called Taylor rule, postulated in the 1990s by John B. Taylor, which ties the interest rate target to inflation and GDP output under/overshoots. Many more variations have been introduced since then that try to incorporate a larger variety of macroeconomic factors (like e.g. effective lower bound constraints and many more). The Fed is currently not following any simple policy rule of this sort and emphasises a rather discretionary approach that allows for more varied and dynamic decision-making based on different market circumstances. The main argument of the Fed against following such rules is primarily their constraining simplicity and inability to capture major economic regime switches. The argument further goes that the purported benefit of straightforward communication would be quickly overshadowed by the necessity for frequent adjustments due to the complexities of our economies.

Policy Tools

After the FOMC decides on the monetary policy objective, regardless of which framework or policy rule was utilized to arrive at it, the Fed’s New York branch takes over. The next step is the implementation of that objective through a variety of policy tools at disposal.

Discount window

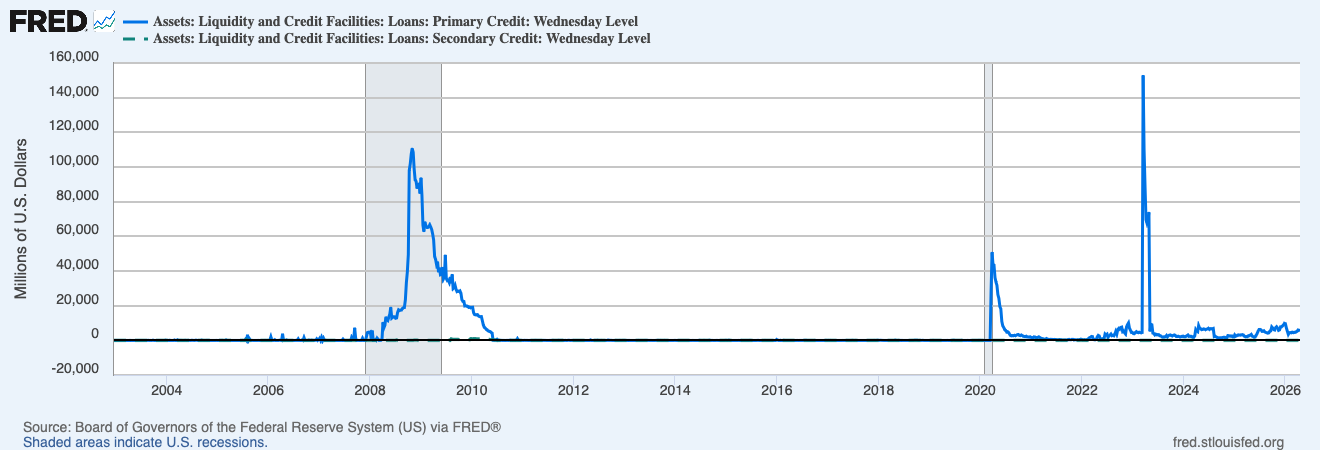

The oldest monetary tool in the toolbox of the Fed is its discount window, a simple lending facility where depository institutions (which includes commercial banks and some other financial institutions) can borrow money in exchange for collateral. This was already introduced in the founding legislation and was regarded as the core tool for solidifying the Fed’s position as a lender-of-last-resort. The discount window has been open to this day and is regarded as one of the tools for ensuring financial stability by guaranteeing to stand ready to provide liquidity into the sector when needed. There are two main rates, the primary and secondary credit rate, that are provided to financial institutions based on their credit and liquidity circumstances. These lending rates are effectively limiting the upper bound at which banks lend to themselves - if they can borrow the money from the Fed for a lower interest rate, there is no reason for them to resort to the inter-bank market for liquidity. This is at least the theory (source). Practically speaking, there has been a stigma associated with using the discount window for a long time. Banks were afraid that by using the window they would signal to other market participants that they might be experiencing financial distress. Even though the individual counterparties are not publicly disclosed until 2 years after the loan was granted, there are more nuanced signals the market participants can use to infer the identity of the borrower. Therefore, banks would rather turn to inter-bank lending facilities, even though they have to pay higher interest on their loans. This stigma has been persisting in the system to some level (see here and here), so there is an ongoing debate about the measures the Fed needs to take to boost the uptake in the usage. Most recent market data has been providing some evidence that the primary window has been seeing some uptick from regular financial institutions (most significantly during the Silicon Valley Bank collapse in 2023), but it’s probably still too early to definitively proclaim its definitive comeback.

The Fed’s primary and secondary credit lines usage since 2002, source: https://fred.stlouisfed.org/graph/?g=1UScu

The Fed’s primary and secondary credit lines usage since 2002, source: https://fred.stlouisfed.org/graph/?g=1UScu

The Fed Funds Rate

At the moment, the discount window is directly set to the upper bound of another of the Fed’s classical tools, and that is the federal funds rate. The naming here is slightly misleading, as the Fed actually doesn’t set this rate directly, but it’s the market rate at which depository institutions provision loan facilities to each other. However, the Fed is able to shift it by injecting or taking liquidity out of the financial system.

To understand how the Fed funds rate works, one must first understand bank reserves and their relationship to the Fed. Depository institutions hold reserve balances at the Fed, which they use to settle payments and meet regulatory requirements. Before 2008, the Fed did not pay interest on these reserve balances, so banks had an incentive to keep excess reserves as low as possible and lend them to counterparties in the overnight market. Because the Fed could change the aggregate supply of reserves in the system, it was able to exert strong influence over the rate at which banks lent those balances to one another.

The way it did that was by purchasing or selling large volumes of short-term T-Bills from depository institutions. These operations basically swap assets and liabilities between the market counterparty and the Fed. When the Fed purchases T-Bills from a counterparty, the asset side of the counterparty changes from the T-Bill to reserve balance. On the other hand, the Fed now holds a reserve balance liability and a T-Bill as an asset. When the Fed sells T-Bills to a counterparty, it eliminates its reserve balance liability by swapping it for the T-Bill that becomes a new asset on the side of the counterparty. What these operations do is inject or take reserves out of the system. Depository institutions react to the shifts in reserve levels by adjusting rates at which they are willing to further lend to each other. If the Fed is purchasing a significant volume of T-Bills, banks will start collecting cash reserves that they are more eager to lend to other institutions, thus pushing the Fed funds rate down. On the other side, if the Fed is liquidating a large portion of its T-Bill portfolio, banks react to the decrease in liquidity by raising the rate at which they are willing to lend between themselves.

These operations constituted the fundamental building block of the so-called corridor or scarce reserve system. It was defined by the Fed moving the levels of reserves in the system with the goal of shifting the interbank market rates. However, this system has undergone fundamental changes since the Global Financial Crisis (GFC).

After Bear Stearns and especially Lehman went into liquidation in 2008, the Fed cut rates quickly and by late 2008 the policy rate dropped to the so-called effective lower bound (0%-0.25%). Funding and credit markets were severely disrupted—unsecured interbank lending shrank and risk premia spiked—so even aggressive reserve provision did not quickly restore normal private credit growth: banks faced capital and risk constraints, not mainly a shortage of reserves. With little room left to ease further via the short rate, the Fed had to start searching for new monetary tools to restore the faith in the financial system and health of the economy.

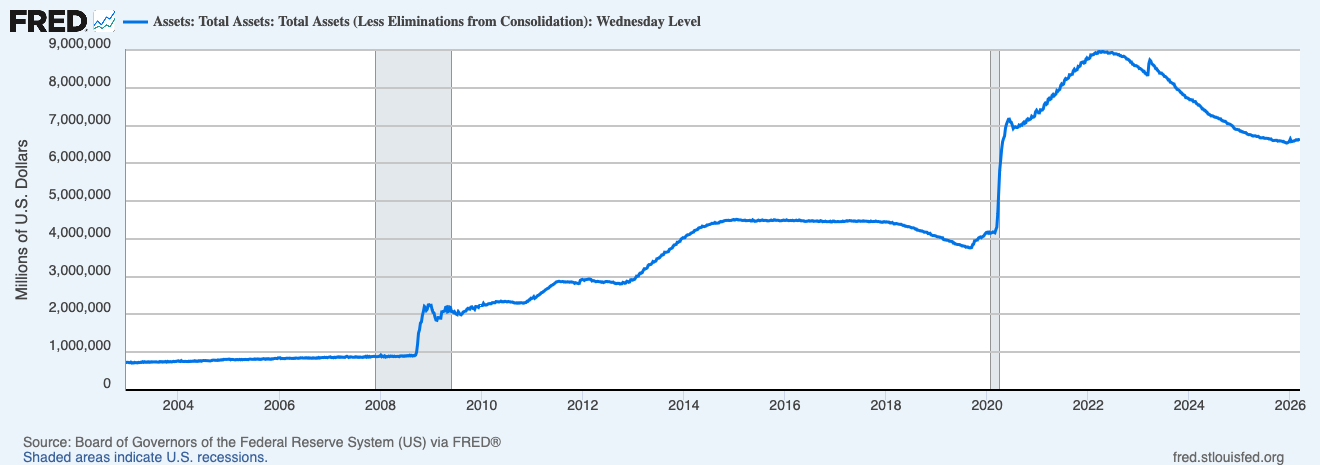

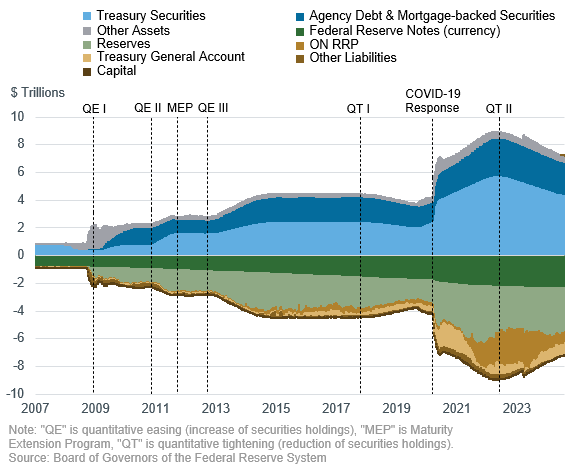

The Fed decided to step into the financial system by injecting significant amounts of liquidity through large-scale asset purchases. This process of so-called quantitative easing (QE) continued in three distinct phases from 2008 until 2014 and targeted primarily mortgage-backed securities and Treasuries. In the beginning, the purported target was removing risky mortgage-related assets from the market and providing enough liquidity for the stressed financial system. In the subsequent phases, the target was improving the weak labor market conditions by pushing long-term interest rates down through enormous purchases of long-term Treasuries. After the US economy started showing significant improvements in terms of inflation and employment targets, the Fed decided to terminate the program at the end of 2014. It resumed significant open market purchases again during the pandemic to stabilize the faltering US economy. Since 2022, it has gradually moved to a process of reversing its balance sheet expansion through rolling off its assets (in addition to selling some of them) called quantitative tightening (QT). However, this process has been much slower than expected and currently the balance sheet is still at around 6.5 trillion US dollars, composed primarily of US Treasuries (around 65%) and MBS (30%).

The Fed’s assets since 2002, source https://fred.stlouisfed.org/series/WALCL

The Fed’s assets since 2002, source https://fred.stlouisfed.org/series/WALCL

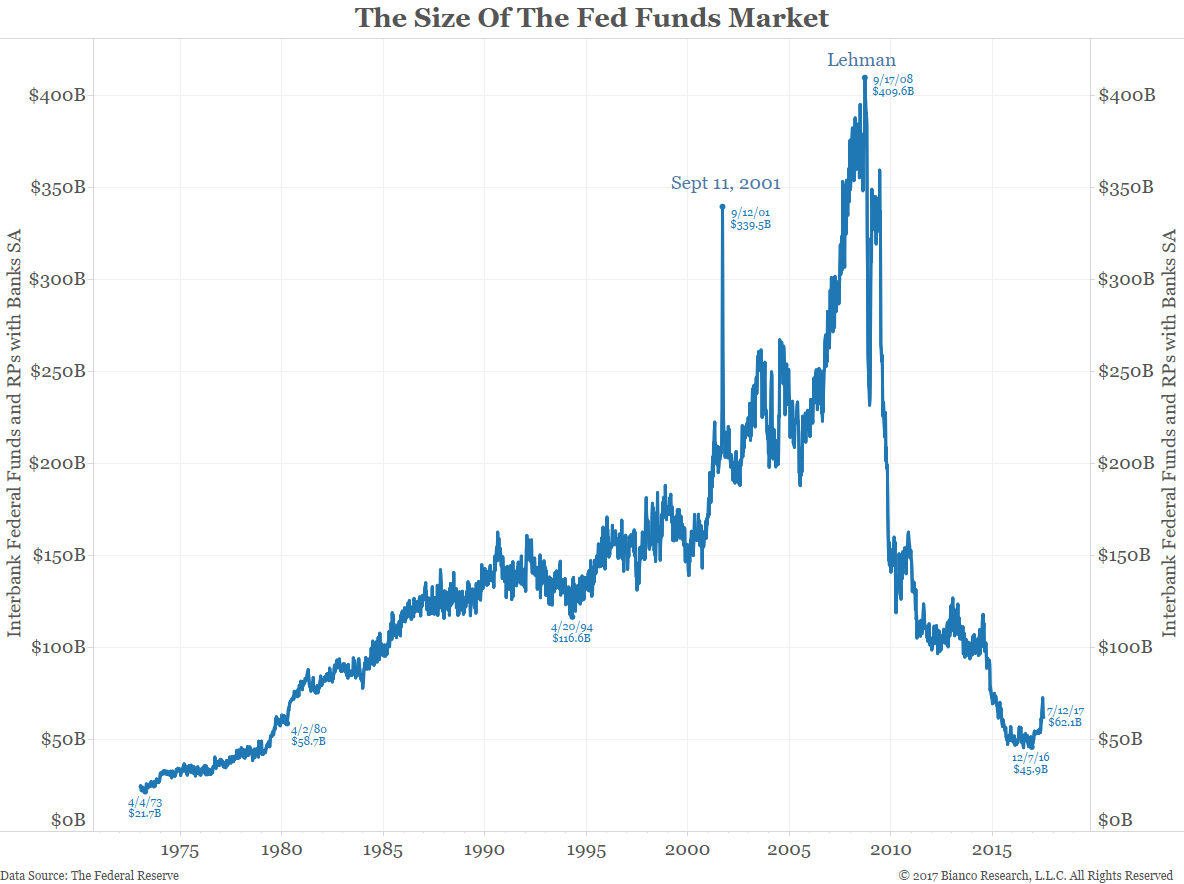

Injecting that much liquidity into the system in the span of the last 15 years did, however, have unintended consequences on the functioning of pre-existing monetary policy tools. Banks gradually stopped feeling the need to borrow liquidity from each other anymore for settlement and reserve purposes as they were already holding enough liquidity. Thus, any additional purchases or sales of short-term Treasury Bills by the Fed won’t move the needle in terms of rates. The corridor system gave way to a floor or an ample reserves system.

Size of the Fed Funds Market, source https://www.biancoresearch.com/what-will-become-of-the-funds-rate-video/

Size of the Fed Funds Market, source https://www.biancoresearch.com/what-will-become-of-the-funds-rate-video/

In the ample reserves system, the interbank money market for reserves is much less critical. Banks hold a sufficient amount of reserves to meet their legal obligations without the need for borrowing in order to fulfill their reserves obligations. Therefore, instead of relying on market pricing through adjusting the amount of reserves in the financial system, the Fed changed its strategy and stepped into the interbank market by setting the rates itself. It’s still borrowing and lending between banks that anchors the effective funds rate, but Fed directly establishes bounds of that rate by using multiple so-called administered rates.

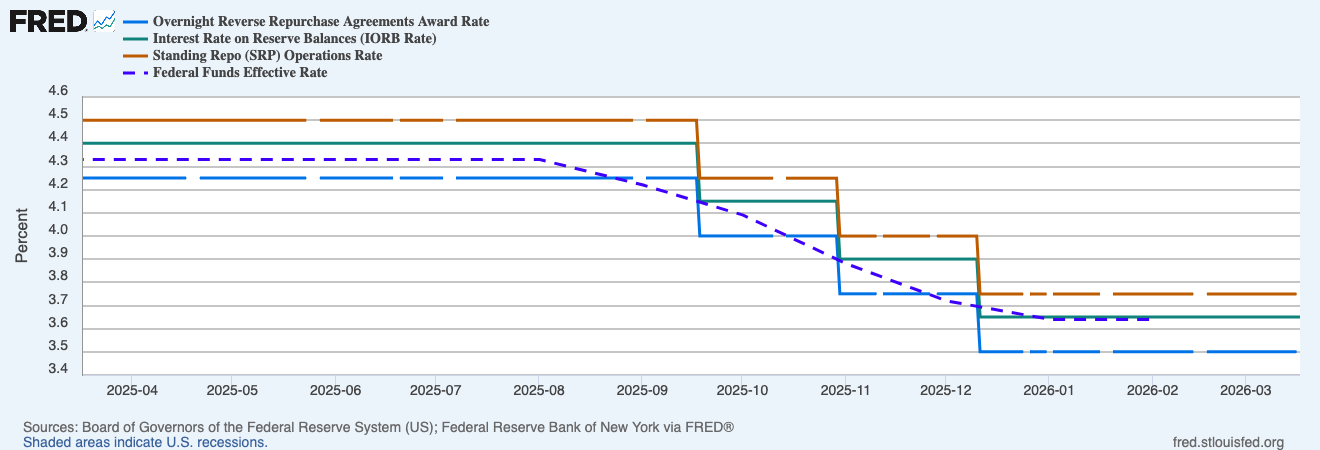

In December 2015, after terminating Phase III of QE, the Fed introduced overnight reverse repurchase agreements (ON RRPs) for a broader range of financial institutions to control the floor of interest rates. These reverse repo operations work by the Fed selling securities to counterparties subject to an agreement to re-purchase the securities at a later date at a higher price. The price difference constitutes the effective interest rate the counterparty is able to capture. It is effectively a collateralized loan to the Fed that removes liquidity from the financial system and helps provide an interest rate floor by providing an alternative investment for a broad base of money market investors (source). The stress on that target audience is especially important. Beginning in 2008, the Fed already offered a competing facility, interest on reserve balances (IORB), to all depository institutions. However, in the US, a significant portion of the financial system is composed of alternative institutions (like money market funds) that don’t have direct access to an account at the Fed, and therefore cannot take advantage of IORB rates. Thus, ON RRPs exist to ensure the Fed’s interest rate targets reverberate throughout wider swathes of the financial system.

In contrast to ON RRP stands the standing repo facility (SRF), where the Fed lends reserves against eligible securities, and thus injects cash into the system by providing a collateralized loan to counterparties. The counterparty is then obliged to re-purchase the security at a later date at a higher price. Again, the price difference is the effective rate the Fed accrues for providing the loan. This facility effectively sets the interest rate ceiling (source). SRF is in a sense a discount window offered for a larger set of counterparties against stricter collateral. In contrast to the discount window, it is intended to be used as a regular, and not just an extraordinary facility.

These three rates are now the cornerstone of the Fed’s toolbox to affect interbank lending rates. They closely track each other, with the lending SRF being the ceiling, IORB mid rate, and ON RRP constituting the floor. The difference between them has been in the range of 10-20 basis points for the past couple of years. The effective Fed funds rate, i.e. the rate at which banks and other financial institutions actually lend to each other, fluctuates within the limits set by these rates.

IORB, ON RRP, SRF, and effective Fed funds rate, since 2025, source: https://fred.stlouisfed.org/graph/?g=1TDR8

There is an ongoing discussion not only among US monetary policymakers, but within the global central bank community, about the merits of the old corridor system compared to the new ample reserves regime. The ample system has been shown to better cushion liquidity shocks that occur in the financial system. Because banks have plentiful sources of reserves, any temporary monetary stress won’t have large spillover or persistent effects. What in the scarce reserves world would possibly cause financial stress and potentially a need for intervention by the Fed is simply avoided by tapping into reserves. Another advantage is the separation between balance sheet operations overall and policy rates. The Fed can keep executing operations in the Treasury markets (for a plethora of different reasons, from Treasury market stabilization to responding to specific crises) without worrying about the impact on the Fed funds rate.

The critics of the ample system lament the large footprint of the central banks operating under the ample reserves system. The Fed currently owns 15% of the outstanding Treasury debt and might resemble more a money market fund than a central bank. This has been shown to potentially cause collateral scarcity in other markets. Additionally, by providing a deposit facility with interest rates where counterparties can park any excess reserves (IORB), the central bank has to pay interest payments to the depository institutions for the reserves it has let into the system in the first place. For 2025, the Fed paid around 167 billion dollars in expense payments, while it only gained 155 billion in interest income from Treasuries and other security holdings (source). Holding interest-bearing liabilities with short duration (mostly overnight loans to the Fed) exposes the Fed additionally to duration risk, as its asset side is largely composed of long-term Treasuries and mortgage-backed securities. Thus, any upward moves in short-term interest rates will force its net interest position into negative territory (as is the case right now). Besides the non-trivial financial implications of suspending remittances to Treasury as a result of paying interest payments to depository institutions, this has obvious political ramifications.

Other tools

The above-mentioned facilities encompass the core of the currently used toolbox of the Fed. They are not all the available tools though. There are some other levers the Fed has a mandate to use - they might be either more targeted to specific institutions, or might have become obsolete by the operating system switch.

The first category of specialised tools contains facilities that deal with the international standing of the US dollar. Because the dollar is effectively the international payment device, controlling and providing liquidity to domestic institutions might be insufficient against a whole breed of risks coming from outside of US borders. In order to avoid any spillovers of foreign dollar strains, the Fed is allowed to act as a lender-of-last-resort for dollars for several international institutions. Central bank liquidity swaps are arrangements through which the Fed provides U.S. dollars to selected foreign central banks. The Foreign and International Monetary Authorities (FIMA) Repo Facility allows foreign official institutions holding U.S. Treasuries to obtain dollars from the Fed by temporarily repoing those securities rather than selling them outright on the market. Both of these tools effectively allow foreign central banks and monetary authorities to obtain dollar liquidity during periods of stress.

In the latter category of largely superseded tools are the Term Deposit Facility (TDF) and the reserve requirement regulation. TDF allows eligible depository institutions to place funds at the Fed for a fixed term in exchange for interest. Functionally, it works similarly to ON RRP or IORB by temporarily draining reserves from the banking system, as balances that would otherwise sit as reserve balances are locked into term deposits for a specified period. Reserve requirements force banks to hold a minimum amount of reserves against certain deposit liabilities. In the older scarce-reserves system, this helped create structural demand for reserves and supported the functioning of the federal funds market. However, since the Fed’s switch to the ample reserves operating system, both of these tools have become functionally inconsequential. TDF has been superseded by ON RRP and IORB, and reserve requirements have been set to 0% as they stopped functioning as a scarcity device.

There is one more tool worth mentioning. Forward guidance is not a balance-sheet operation or a standing facility, but a communication tool. It works by the Fed shaping expectations about the future path of short-term interest rates, asset purchases, or the overall stance of policy. Because longer-term interest rates partly reflect expectations of future short-term rates, clear guidance from the Fed can influence financial conditions even when the current policy rate is unchanged.

This tool became especially important after 2008, when policy rates were pushed to the effective lower bound and conventional easing had limited room left. By signaling that rates would remain low for an extended period, or that policy would stay supportive until certain macroeconomic conditions were met, the Fed attempted to lower longer-term yields and support spending, investment, and employment.

Balance Sheet

The Fed’s balance sheet evolution, source: https://tellerwindow.newyorkfed.org/2024/08/06/the-role-of-the-federal-reserves-balance-sheet-in-monetary-policy-implementation/

The Fed’s balance sheet evolution, source: https://tellerwindow.newyorkfed.org/2024/08/06/the-role-of-the-federal-reserves-balance-sheet-in-monetary-policy-implementation/

Now that we have a good understanding of the Fed’s policy tools and their evolution, the composition of its balance sheet should not come as a surprise.

As of 2026, as a result of the QE programs of the early 2010s and 2020s, the asset side of the Fed’s balance sheet is heavily dominated by Treasury securities of varying maturities, and mortgage-backed securities issued by government agencies. The Fed additionally holds a small proportion of foreign currency-denominated securities, gold certificates, and finally loans to depository institutions. These are either in the form of discount window lending or SRF.

On the liabilities side, the biggest item is the reserves of depository institutions held at the Fed. These are used by banks to settle payments, to support their liquidity risk management, and satisfy regulatory requirements. After that comes currency, and further down sit securities obligations in the form of ON RRP. Treasury’s General Account, which is used to manage Treasury’s cash position, including to make and receive payments related to taxes, spending, and the issuance and repayment of Treasury-issued debt, is another non-negligible item. And finally, like any other bank, the Fed also holds equity provided by individual member banks.

Transmission of Monetary Policy

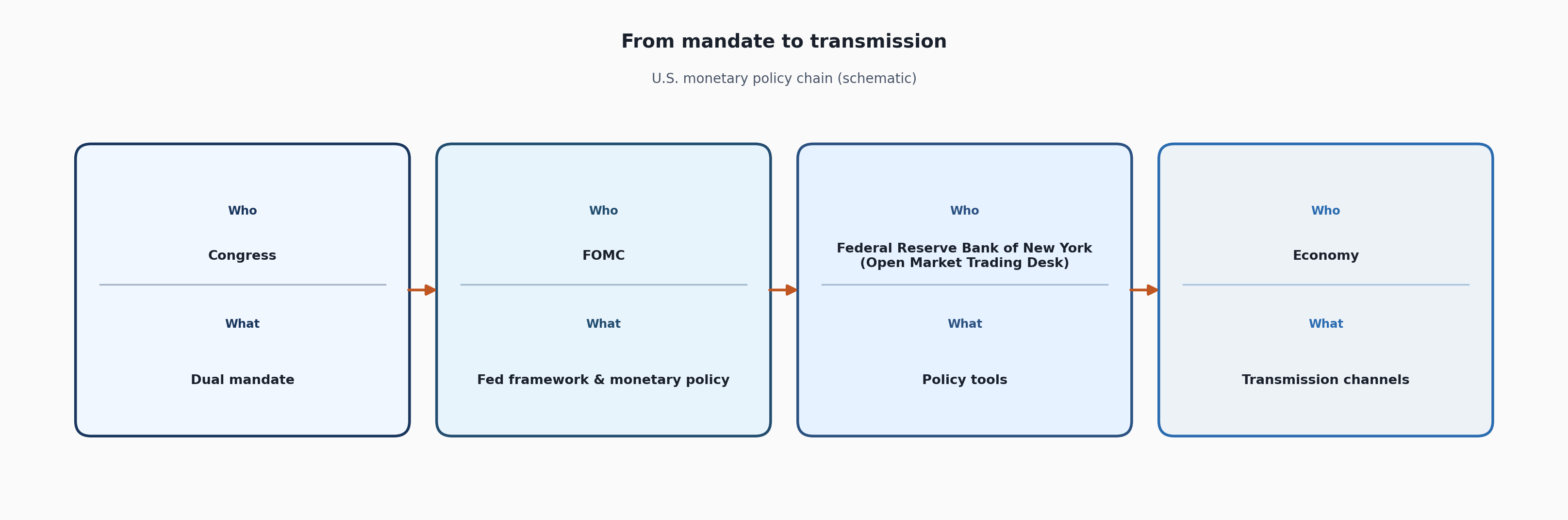

Chain from statute to real economy

Chain from statute to real economy

After the Congress decides on the Fed’s mandate, the Fed’s FOMC is responsible for the framework of how to align that mandate with real-world economic circumstances through targeting short-term (through the Fed funds rate) and long-term (through QE) interest rates in the economy. The Fed’s New York Trading Desk then uses available policy tools to achieve FOMC’s target. The final leg of the puzzle is what happens once these targets are successfully implemented: how do they translate to price stability and employment outcomes? This is the basis of the monetary transmission mechanism.

There are different channels through which the Fed’s monetary policy can affect the real economy. The interest-rate channel works through changing the expectations of businesses and households on the trajectory of current and future short-term rates. It then moves through the financial system reflecting the rate change in its own pricing of loans, which, by implication, changes the investment and borrowing decisions of households. The already-mentioned forward guidance, introduced largely by Ben Bernanke, helps to further solidify expectations of future rates among actors in the economy.

Large-scale open market operations, championed during quantitative easing, directly shape the long-term yields on safe assets through the so-called portfolio rebalancing channel. By purchasing significant amounts of government bonds and mortgage-backed securities, the Fed lowers the yield on these securities. Investment actors thus cannot guarantee the previous rate of return under the same risk profile, and must change their portfolio composition to adjust. They do that by allocating more portions of their capital into riskier assets, be it corporate or municipal bonds, or equities, thus spurring more investment into the economy.

Conclusion

The role of the Fed and its impact on the economy have been in constant shaping since its founding in 1913. It started as a central federal lender-of-last-resort with the mandate to help command the US financial system through turbulent times. Since then, it accumulated additional responsibilities, the most critical of which is steering the country’s price and employment conditions. For the majority of the 20th century, this was achieved via controlling the Fed funds rate by adjusting reserve supply in a so-called corridor system. This regime underwent fundamental changes as a result of the necessity to react to the GFC, when the Fed decided to unleash massive open market operations as part of the quantitative easing programme. The repercussions of this policy meant that the Fed had to soon embrace a more direct approach to controlling interest rates in the new regime of ample reserves.

In addition to being the core of the US financial system, it has gradually cemented its role as a center of the international dollar market through its crisis foreign swap programs. Under Chairman Ben Bernanke, it additionally underwent strategic internal changes that can be seen in its more outward communication presence through the so-called forward guidance and bigger stress on formalisation of its approach to monetary policy through regularly reviewing and disclosing the Fed’s framework.

Additional sources:

- Organisational structure of the Fed: https://www.moneyandbanking.com/commentary/2025/9/13/fed-division-of-powers-who-controls-monetary-policy

- Monetary Policy Tools: https://www.federalreserve.gov/monetarypolicy/policytools.htm; https://www.newyorkfed.org/markets/domestic-market-operations/monetary-policy-implementation

- The Fed’s balance sheet: https://www.federalreserve.gov/aboutthefed/audited-annual-financial-statements.htm; https://www.federalreserve.gov/econres/notes/feds-notes/a-brief-illustrated-history-of-the-federal-reserves-balance-sheet-20260213.html

- Monetary policy transmission: https://www.federalreserve.gov/monetarypolicy/monetary-policy-what-are-its-goals-how-does-it-work.htm